Have Taxes Kicked Your Ass(ets)?

You're about to discover the secret of paying less taxes to Uncle Sam so that you can build wealth.

After taking a short quiz and reading this blog post, you'll receive a Free Case Study that explains 3 bullet-proof wealth-building secrets that I've developed after a 20-year career in financial services. I'm also throwing in a free complimentary tax review to save you even more.

Just to recap, all you have to do is:

1. Take the quiz.

2. Read the post.

3. Download the study.

1-2-3. Just that easy. Are you ready?

Question #1: What does a tax refund represent?

Question #2: If you include income from ALL sources, how much did your household earn last year?

Question #3: Do you regularly contribute the annual limit to retirement plans offered by your employer?

Question #4: Are you eligible to make Roth IRA contributions?

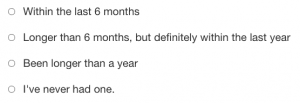

Question #5: When is the last time you've had a tax planning meeting?

Question #6: Are you eligible to make after-tax contributions to your retirement plan?

Question #7: When is the last time you've had a benefits review? (e.g. all the stuff your employer offers when you first get hired)

Question #8: Do you prepare your own taxes?

Question #9: If I could show you a way to reduce your tax liability by at least $5,000 in one phone call, would you be interested?

Here’s the deal.

After more than 20 years in financial services and 24 years of marriage (and 3 adult children), I know one thing for sure…you don’t know what you don’t know.

Further, being confident around your ignorance is a recipe for disaster. And let me tell you from experience there’s nothing worst than being caught with your pants down (proverbially speaking) during an IRS audit. This is how you really get taxes to kick your ass(ets).

But there is a remedy for this. It has to do with being proactive in your tax planning.

What is proactive tax planning?

It's simply the act of taking control of your taxes.

If you don't own it, then someone else will (e.g., financial institution, tax preparer, or worst--Uncle Sam).

And no one wants to let those folks have a crack at their money without being involved in the process.

Ok, ok...enough said. Let's get into the gory details of proactive tax planning so you can avoid making mistakes (which by-the-way are very common).

The best way I know how is by breaking down each step into bite-size pieces.

Understand the tax formula

Conduct a tax analysis

Create a customized tax strategy

Understand the formula to lower your taxes

The tax formula is actually a very simple thing to understand.

Here's the problem though...the tax code is several times longer than the Bible, with more words in it than any novel other than War and Peace-in English at least.

You have line items to consider, schedules to fill out, filing statuses to consider, etc.But with all that, it is a really simple equation...

Income from all sources

Less adjustments (i.e. Contributions to retirement, self-employed health insurance, student loan interest, amongst other things)

This will give you Adjusted Gross Income (e.g. AGI)

Less deductions (you can apply the higher of the standard deduction or itemize with things like mortgage interest, real estate taxes, charitable giving, amongst other things)

This will give you Taxable Income. ***Note: This is the number used to determine your tax liability.***

Your tax liability is then further adjusted by any:

Tax credits/payments (including withholding from your paycheck or estimated tax payments)

A positive number means you get a refund, a negative number means you owe.

By understanding this formula, you now know that your ability to lower taxes comes in the following areas:

your ability to reduce taxable income, by

increasing deductions or applying negative adjustments to gross income

I commonly see individual returns where people fail to claim one of the many exclusions available to you to reduce taxable income. This causes you to overpay through a combination of not claiming deductions and tax credits that you're entitled to.

To save yourself from this mistake, you need a tax analysis.

Conduct an analysis to lower your taxes

What does conducting a tax analysis look like?

To be honest, it will be hard for you to spread your tax returns on the kitchen table and do this--it just is what it is.

So instead of trying to do your tax analysis like this...

You should aim for something like this...

Since the last picture is a screenshot of some expensive software that financial professionals like myself use, you will likely need to include a professional at this point.

But before you think I'm saying that just so you can pay someone for this service (I do this for free BTW), hear me out.

There's value in just getting a different perspective on something.

Excuse the following analogy...

Imagine you're diagnosed with a terminal disease by your primary care physician. Wouldn't you get a second and maybe even a third opinion on the situation to offer a different perspective?

This is the purpose of having a financial professional conduct a tax analysis for you.

Now all financial professionals will not offer this if they are not qualified in this area, so make sure you select someone that is competent in taxes.

Specifically, you'll be looking for feedback on the following:

How different filing statuses can affect your tax liability. Typically, married couples benefit from filing jointly, but there are a few times where this isn't the case and since you can always change your status, it's worth exploring.

How bundling itemized deductions in different years can affect your tax liability. Did you make a big charitable contribution in a particular year? For example, consider a married couple that donates $9,000 to charity each year. This $9,000 donation will not create an additional tax benefit if their total deductions do not exceed the standard amount (currently set at $24,000). However, by saving up several years’ worth of donations and making a bigger donation in a single year, they can itemize in that year and receive a tax benefit for their donation.

How lowering AGI and MAGI affects your eligibility for other contribution opportunities. Lowering your adjusted gross income and your modified adjusted gross income affects your ability to make Roth IRA contributions which affect the amount of tax-free income you'll have in the future.

There are more points of analysis but you're getting the picture, right?

Create a customized strategy to lower your taxes

Finally, you should create a customized tax strategy to allow you to reduce your tax liability (potentially).

I say potentially because there are multiple points of analysis and different individual constraints to be explored that present possibilities for you to lower the amount of taxes you pay.

Again, you don't know what you don't know.

The tax strategy you create may (and will) change from year to year depending on what is uncovered with a thorough tax analysis during annual reviews.

Perhaps you have a low-income year and it makes you eligible to make Roth IRA contributions whereas you previously weren't. Perhaps you change jobs and are able to make after-tax retirement contributions and this has a cascading effect on other elements of your tax strategy.

There are many factors (or levers as I like to call them) that can help you put together a strategy that will not have you paying more than your fair share in taxes.

Ultimately allowing you not to have taxes kick your ass(ets)!

Now that you've finished your reading homework for today🤣, you may want the FREE case study I promised earlier.

All you need to do is enter your email here and I'll send it to you.